Behind on Mortgage Payments? Your Complete Guide to Help and Foreclosure Avoidance

- Scott Westfall

- Apr 20

- 11 min read

Have you ever wondered if there was a way to stop the foreclosure clock even after missing a few payments? Whether you’re in a family home in Kempsville or a rental near the Virginia Beach Oceanfront, the stress of falling behind is the same.

Life can hit hard, and even responsible people can fall behind on their mortgage payments due to unexpected hardship. But there is hope – there are immediate steps you can take to avoid foreclosure. The key is acting fast. In this complete guide on what to do when behind on mortgage payments, we’ll help you find the help and options you need.

What to Do First When You Fall Behind on a Mortgage

What happens when you fall behind on your mortgage? Who needs to know? How far behind on mortgage payments can you be before foreclosure occurs? Let’s break it down.

Note: There are special foreclosure rules for loans like VA, FHA, or reverse mortgages. Contact your lender as soon as you suspect you’ll miss a payment to make sure you get the full picture for your loan.

Who Should You Call?

The very first thing you want to do when you find yourself falling behind on mortgage payments is to call your loan servicer.

It may feel intimidating to admit you’re not going to make a payment, but servicers prefer to work with homeowners rather than foreclose on a property when possible. The overall loan delinquency rate in Q1 of 2025 was 4.04%, which means about one in 25 loans had missed a payment. They have a process for helping you catch up.

Have any helpful documentation ready when you call, including:

Mortgage loan account number

Your latest monthly mortgage statement

Co-borrower information, if applicable

Proof of income

Hardship letter stating why you are unable to pay, and whether the problem is temporary or permanent

It can also be a big help to have your most recent bank statements, tax returns, income documentation, and estimated monthly expenses on hand for the conversation.

In Virginia, it can also be helpful to have a copy of the deed and trust and any foreclosure notices you received if you’re already concerned about foreclosure.

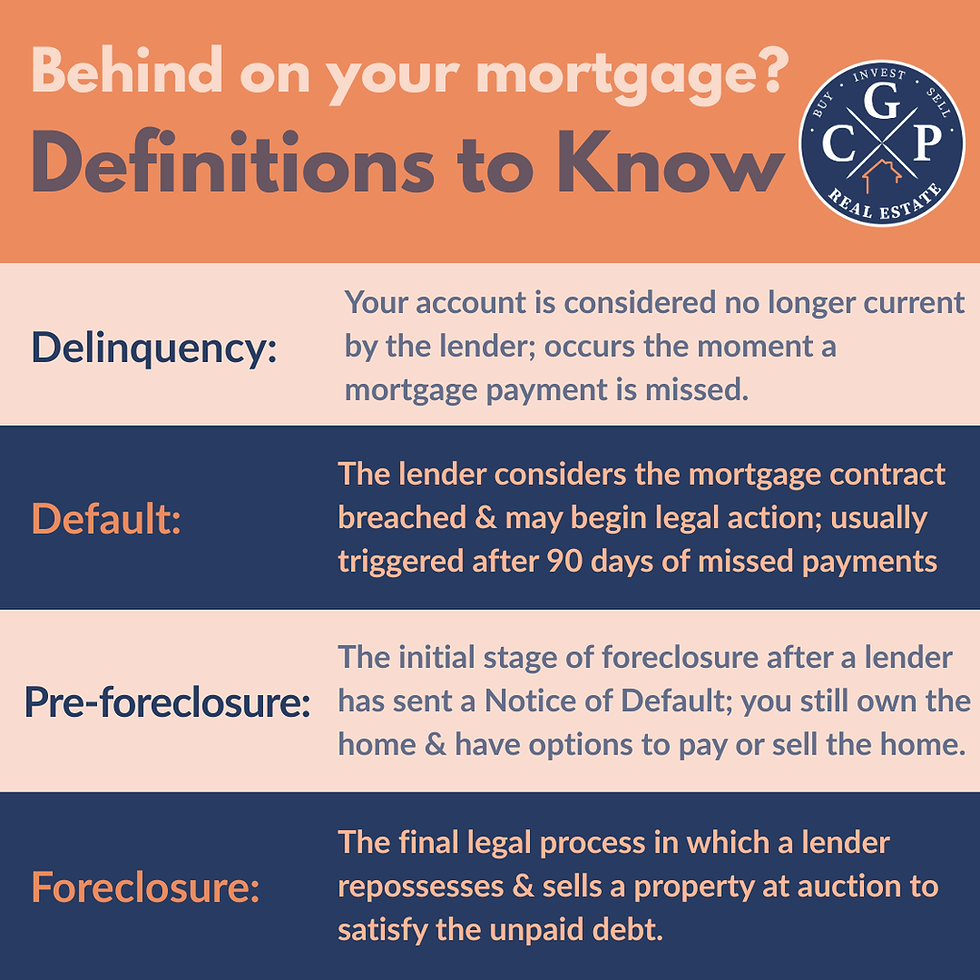

What Happens When You Fall Behind on Your Mortgage?

If you miss a mortgage payment, that doesn’t automatically mean that the loan company can foreclose on your house. However, that first missed payment starts a series of events that escalate in severity the longer you are behind on your mortgage.

If you remain delinquent, you’ll begin to get late fees, your lender will start making contact, your account could enter default, and your credit score could be seriously damaged.

If you miss at least three payments, your lender will likely send a Demand Letter or Notice of Intent to Accelerate your loan – which means the entire loan balance will come due immediately, not just the past-due balance.

After about four months (depending on your state), the foreclosure process will start, and you could lose your home.

What’s the Timeline When You Are Behind on Your Mortgage?

How many months can you fall behind on your mortgage before foreclosure?

Before anything drastic happens to your loan or property, there are grace periods and timeline milestones that need to be met. Foreclosure timelines vary by state, so make sure to research the timeline for your state. As an example, we’ll break down the foreclosure timeline for Virginia.

Virginia is primarily a non-judicial foreclosure state, so the process generally occurs outside of the court system, making it much faster than in many other states.

Timeline | Key Event | Description |

Day 1 | Missed Payment | Your mortgage payment is officially late. |

Day 16+ | Late Fee Assessed | Most lenders will apply a late fee, as specified in your loan agreement. |

Day 36 | Required Contact | Your loan servicer must attempt to establish live contact (phone call) to discuss loss mitigation options. |

Day 45 | Written Loss Mitigation Notice | The servicer must send a written notice detailing available options to avoid foreclosure, such as loan modification or forbearance. |

Day 90+ | Notice of Default / Acceleration | Your lender will likely send a formal letter (Breach Letter) that states the loan is in default and warns that the full outstanding balance (acceleration) will be demanded unless the default is cured by a specific date. |

Day 120 | Foreclosure Can Begin | Under federal law, the servicer cannot formally start the Virginia foreclosure process until your account is at least 120 days delinquent. This time is intended for you to submit a loss mitigation application. |

In Virginia, the action and foreclosure process can move pretty quickly after the 120-day mark. The trustee or lender will provide a notice of sale at least 60 days before the public auction if the residential home is owner-occupied.

Can I Keep My House or Do I Need to Foreclose?

The next immediate step is to evaluate your financial standing. Is the hardship you’re facing temporary, or will it likely take some time to resolve? Having a clear and honest view of your budget, both in the short and long term, can help determine whether you can keep your house.

Foreclosure Prevention Options to Keep Your Home

You have options when behind on mortgage payments. Lenders often offer a few loss mitigation solutions to get you back on track with payments and prevent foreclosure on your home by adjusting your payment structure.

Forbearance

Forbearance allows you to temporarily pause or reduce monthly mortgage payments. It’s often a good option for short-term financial hardship when you expect your income to stabilize soon. Lenders usually agree to 3-12 months of forbearance, but the missed amounts need to be repaid later through a lump sum, repayment plan, or a deferral added to the loan.

Repayment Plan

If you missed a few payments but have since resolved your financial hardship, a repayment plan allows you to catch up on missed payments a little each month. Your total past-due amount is divided, with a chunk added to your standard monthly mortgage payment over a fixed period – often 3-6 months.

Loan Modification

If you need a long-term mortgage assistance solution due to a more permanent hardship, a loan modification allows you to restructure your original loan terms permanently. Your lender works with you to make your monthly payments more affordable long-term, usually through reducing your interest rate, extending the loan term, or adding the missed payments to the total principal balance. It’s an option to catch up on mortgage payments and keep your home.

Refinancing

A common question is: “If I’m behind on my mortgage payments, can I refinance?” It might be an option for you.

Refinancing involves replacing your current mortgage with a brand-new one. However, it’s only viable if your loan delinquency is minimal (or you haven’t missed payments yet) and your credit is still good. You can seek a lower interest rate, but you also have to qualify under current market conditions and may have to pay closing costs.

If you’re behind on your mortgage but want to keep your home, it’s imperative you seek free professional help. Confidential assistance is available at no cost from HUD-certified housing counselors.

Here are a few local Virginia Beach and Hampton Roads resources for those navigating loss mitigation options:

When You Need to Sell: Short Sale vs. Deed-in-Lieu vs. Cash Offer

When it seems you can’t catch up on your mortgage payments before foreclosure, you still have some options to sell your home to resolve your debts and avoid the stress and credit damage of foreclosure by your lender.

When pursuing any of these, it’s important to consult with a qualified real estate agent in your area (here’s some in Hampton Roads), a foreclosure attorney or housing counselor, and a tax professional to make sure you understand the financial and legal implications.

Being behind on your mortgage and foreclosure don’t have to be synonymous. Let’s look at some different ways you can sell your property to avoid foreclosure:

Short Sale

A short sale is the sale of a home for less than the mortgage balance. This requires approval from the lender.

Pros of a short sale:

You avoid foreclosure.

The damage to your credit score is less than foreclosure.

You have a shorter waiting period for a new conventional mortgage than after foreclosure.

You maintain ownership and the right to live in the property until the sale closes (usually).

Your lender typically pays closing costs, transfer taxes, and real estate agent commissions for the sale.

Cons of a short sale:

Your credit still takes a hit and will be marked with the short sale for up to 7 years.

Your lender has to agree to every detail, making the process lengthy and often stressful.

You still have to go through the process of selling the home.

Any forgiven debt may be considered taxable income.

Lenders may pursue a deficiency judgment, requiring you to pay the remaining debt.

You forfeit any remaining equity in the property and receive no proceeds from the sale.

In the “recourse state” of Virginia, lenders have the legal right to sue for a deficiency judgment after a foreclosure. If you are pursuing a short sale, you must get a written agreement from your lender to waive this deficiency to avoid being sued later.

Deed-in-Lieu of Foreclosure

Getting a deed-in-lieu of foreclosure is when a homeowner voluntarily transfers the deed of the property to the mortgage lender to cancel the debt.

Pros of a deed-in-lieu:

You avoid foreclosure.

The credit hit isn’t as severe as that of a foreclosure.

It may be easier to qualify for a new mortgage sooner than if you foreclose.

Lenders usually agree to cancel the entire mortgage loan, including the deficiency balance.

No selling effort is required on your end, unlike a short sale.

Sometimes, lenders offer a small amount of relocation assistance to encourage a smooth and timely handover of the property in good condition.

Cons of deed-in-lieu:

Your credit score still takes a hit and will be marked for up to 7 years.

Forgiven debt may be considered taxable by the IRS.

Lenders don’t have to agree to a deed-in-lieu.

Other existing liens, like tax liens or a second mortgage, make these less likely to secure with a lender.

You forfeit any remaining equity in the property and receive no proceeds from the transaction.

You have to move out by a specified deadline and lose ownership rights when the deed is transferred.

Note: If your lender agrees to forgive the deficiency balance during a short sale or deed-in-lieu agreement, make sure to get it in writing.

Sell Your House Fast for Cash: The CGP Cash Buyer Offer Program

If you need speed and certainty with cash in hand, selling your house to a cash buyer can be the best path forward. It also tends to be the fastest and easiest solution, as you can sell the property as-is.

Pros of selling fast for cash:

It’s the fastest way to sell your home, usually closing within two weeks.

You’re more likely to beat a foreclosure deadline because the buyer doesn’t rely on financing, appraisals, or long underwriting processes.

You avoid the financial and credit damage of a foreclosure.

No repairs, cleaning, or staging are generally required, saving you time and money.

It’s generally a streamlined process without middle-man agents.

Buyers typically pay the closing costs.

You can negotiate a flexible closing date or short leaseback period to give you more time to relocate.

Cons of selling fast for cash:

If you owe more on your mortgage than you can get from a cash sale price, you’ll still owe a deficiency balance and need the lender’s approval for the sale price to clear your mortgage.

There’s not a lot of leverage for cash sales price negotiation when you sell as-is.

Typically, you’ll be selling below market price .

Some predatory investment companies target homes at risk of foreclosure. Be wary of high-pressure buyers who try to lower the price last minute or charge unexpected upfront fees.

(The family-owned CGP Cash Offer program in Virginia was designed to protect those needing to sell fast for cash. We present owners with options specific to their situation. Learn more here.)

If you’re at risk of foreclosure, a cash offer is a way to find certainty and ease in the midst of the stress.

CGP Real Estate has a cash offer program in Hampton Roads, Virginia. Get a fast, no-obligation cash offer today.

The Bottom Line

If you’re behind on your mortgage and looking for options and assistance, the power is in your hands if you act now. Take control of your situation by understanding the terms, options, and action steps outlined in this complete guide to help when falling behind on mortgage payments.

To keep your home, work with your servicer to learn your options for mitigating the loss of your home.

If selling your home before foreclosure is the most realistic path for you, consider the options of a short sale, deed-in-lieu, or taking advantage of a cash offer for your home.

Ready for a simple, quick solution for a Hampton Roads house with a mortgage? See if you qualify for a no-obligation cash offer now.

FAQs on Falling Behind on Your Mortgage

How many months can you fall behind on your mortgage before foreclosure starts?

In most cases, including Virginia, federal law prevents a loan servicer from officially starting the foreclosure process until you are at least 120 days (4 months) delinquent. This window is designed to give homeowners time to apply for loss mitigation options. However, your lender will likely send a "Notice of Intent to Accelerate" after 90 days of missed payments.

What is the difference between mortgage delinquency and default?

Delinquency occurs the moment you miss a single mortgage payment; your account is simply no longer current. Default is more serious and is typically triggered after 90 days of non-payment. At this stage, the lender considers the mortgage contract breached and may begin legal action to accelerate the loan.

Can I sell my house if I am behind on mortgage payments?

Yes, you can sell your house during the pre-foreclosure period as long as the sale is completed before the final foreclosure auction. Options include a traditional sale (if you have equity), a short sale (if you owe more than the home is worth and have lender approval), or a fast cash offer to meet tight foreclosure deadlines.

What should I do first if I can’t make my mortgage payment?

The first step is to contact your mortgage loan servicer immediately. Do not wait until you have missed a payment. Servicers often have loss mitigation departments specifically designed to help you explore options like forbearance or loan modification. You should also gather your financial documents, including proof of income and a "hardship letter."

What is a "Deed-in-Lieu" of foreclosure?

A deed-in-lieu of foreclosure is a voluntary agreement where the homeowner transfers the deed of the property to the lender to satisfy the debt and avoid the foreclosure process. While it still impacts your credit score, it is often less damaging than a formal foreclosure and may eliminate your responsibility for the deficiency balance.

Does Virginia require a court hearing for foreclosure?

Virginia is primarily a non-judicial foreclosure state. This means the foreclosure process generally occurs outside of the court system, allowing it to move much faster than in judicial states. Because of this speed, it is critical for Virginia homeowners to act quickly once they receive a Notice of Default.

What are the pros of selling to a cash buyer to avoid foreclosure?

Selling to a cash buyer like CGP Real Estate offers speed and certainty. Benefits include:

Speed: Closing can often happen within two weeks, potentially beating a foreclosure deadline.

No Repairs: Houses are purchased "as-is," saving you the time and money required for cleaning or staging.

Simplicity: There are no bank appraisals or lengthy underwriting processes that could delay the sale.

Where can I find free help if I’m facing foreclosure in Hampton Roads?

Homeowners in Virginia Beach and the surrounding Hampton Roads area can access free, confidential assistance from HUD-certified housing counselors. Credible local resources include:

The Up Center

Catholic Charities of Eastern Virginia

Urban League of Hampton Roads

Legal Aid Society of Eastern Virginia

Can I keep my home if I’ve already missed three payments?

Yes, it is possible to keep your home through loss mitigation. Options include loan modification (restructuring your loan terms), a repayment plan (catching up over several months), or forbearance (temporarily pausing payments). You must submit a complete loss mitigation application to your lender to be considered for these programs.

What is a deficiency judgment?

A deficiency judgment is a legal ruling allowing a lender to sue a borrower for the remaining balance if the home sells for less than what is owed at a foreclosure auction. Since Virginia is a "recourse state," it is vital to get any agreement to waive a deficiency in writing when pursuing a short sale or deed-in-lieu.